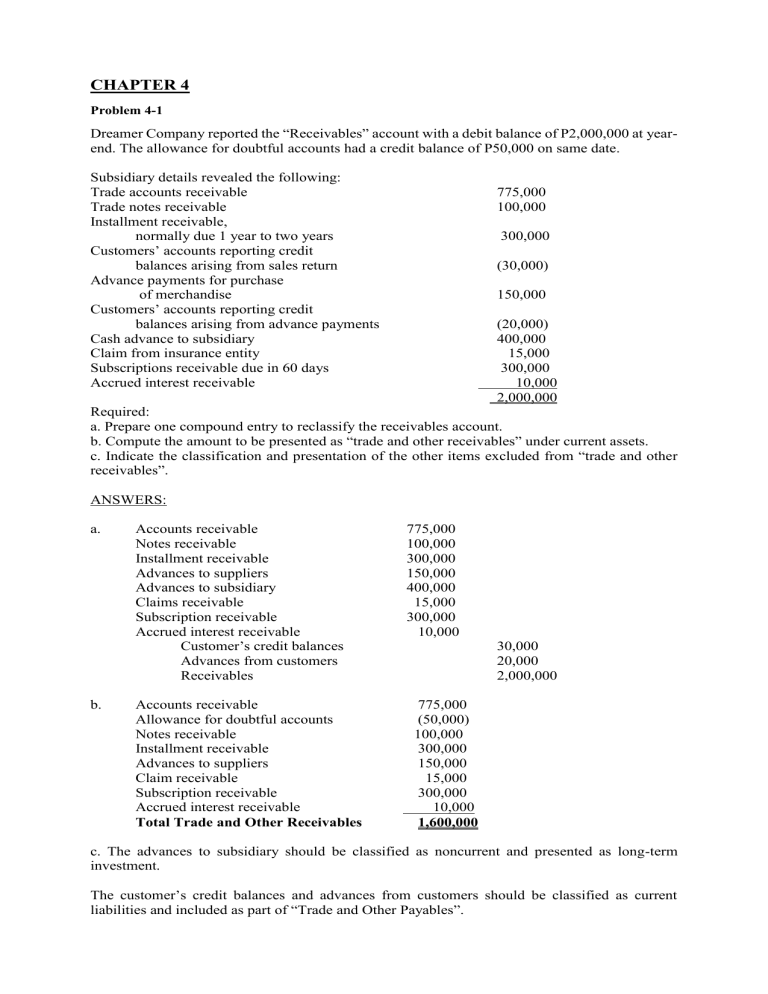

Regulators department-supported loan applications are great options for earliest-day homeowners or all the way down-earnings borrowers. USDA and FHA finance is one another work on of the some other bodies companies and can feel simpler to qualify for than other traditional home loan applications.

When you compare USDA and you will FHA loans, you’re not really much better than another; the loan program that’s right for you will depend on their newest problem. One another USDA and you can FHA home loan money bring several differences one to make them popular with earliest-time homebuyers and you may low- so you can moderate-money borrowers.

Just like the the leading Kansas Urban area mortgage lender, Earliest Fidelis helps make the latest lending process easy for your. Our USDA and FHA finance are created to create real estate and refinancing alot more affordable. This is what you must know throughout the FHA and you may USDA funds in Kansas Town.

What is actually good USDA Loan?

USDA financing are offered by personal loan providers and you will backed by brand new You.S. Agency out-of Farming. Having USDA fund, consumers need satisfy particular money and you may location conditions because these financing are merely accessible to those residing being qualified rural groups.

While the procedure for taking a great USDA loan can take extended than an FHA mortgage, its because USDA loans have to be underwritten double. Generally speaking, the lending company often underwrite the mortgage earliest, and then it could be underwritten again because of the USDA. Although not, when you have a credit rating from 640 or maybe more, the loan are immediately underwritten of the USDA without more time on it.

Benefits of a beneficial USDA Loan

USDA home lenders could work to you to obtain the prime loan system to suit your novel condition. An effective USDA loan also offers benefits so you can home buyers, including:

- No advance payment requirement

- Reduced financial insurance rates and you can charge

- The seller can pay one closing costs

- Commonly less expensive than an enthusiastic FHA mortgage, each other upfront and you will lasting

- Lenders may well not require you to features bucks supplies so you’re able to secure one money selection

- No borrowing limit; restrict loan amount utilizes your capability to repay

USDA Financing Qualification Requirements

USDA mortgages are supposed to raise homeownership pricing as well as the economic climates for the outlying section. Hence, you need to live in a professional rural urban area to take advantage of a great USDA financing. Your local area must also see specific county assets qualification criteria.

USDA loans have other qualifications conditions too. Your credit rating must be at the least 640 or even more, while must have a pretty reasonable obligations-to-income ratio-as much as fifty percent of your money or reduced.

Fundamentally, USDA financing possess rigorous earnings height guidelines. These can differ according to the number of individuals on your own domestic while the precise location of the family. Should your income is more than 115 per cent of one’s average earnings because urban area, you will be ineligible and should not be eligible for an excellent USDA loan.

What’s an enthusiastic FHA Mortgage?

A keen FHA home loan is actually backed by new Government Property Management and you can considering by way of personal lenders. If you’re an FHA financing process usually takes more hours than simply a USDA loan, it’s a great amount of independency to own homebuyers with all the way down fico scores.

However, payday loan Groton Long Point FHA home loan conditions do establish an optimum financing count built on your own location, so it’s important to keep this in mind as you store to possess land.

Benefits associated with a keen FHA Mortgage

- Demands a credit score out of 580 or more, it is therefore ideal for those with all the way down borrowing

- Zero earnings standards or restrictions

- Large personal debt-to-income ratio greet

FHA Loan Qualifications Criteria

Just very first-day homebuyers is recognized getting a keen FHA financing. And also this is sold with consumers whom haven’t possessed a home when you look at the at the very least 3 years.

While you are there are not any earnings standards getting FHA financing, you are going to need to prove your income matter and feature one you possibly can make monthly mortgage and insurance rates costs. FHA money and support increased debt-to-money proportion, particularly if you has actually a top credit rating.

If you are a first-date home consumer otherwise seeking to re-finance, Earliest Fidelis is here to assist. We offer our very own customers USDA and you can FHA mortgage options, so our very own specialist loan providers will find the right loan program to possess you. Get started with the pre-recognition app, or e mail us today at the 913-205-9978.